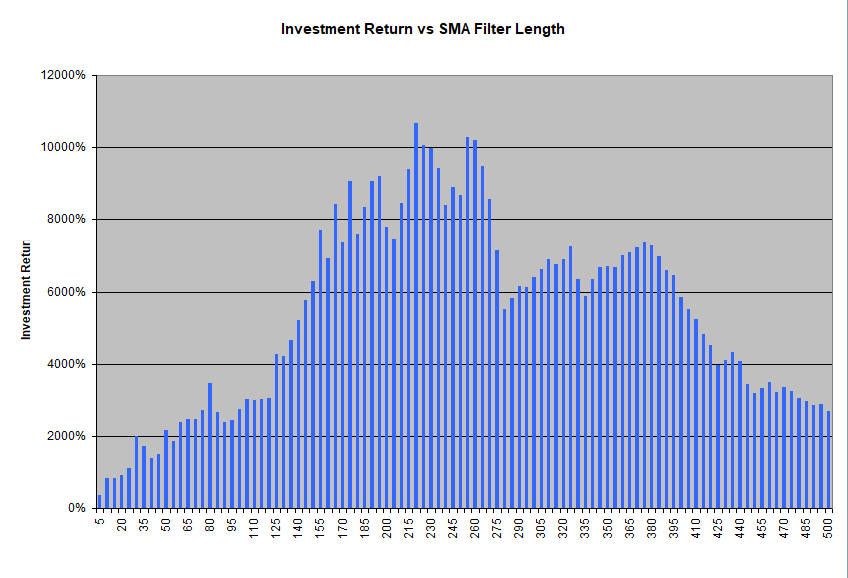

In our post the Quantitative Process – Part I we discussed how we can improve our Risk Return on our investment in the S&P 500 by using a simple moving average filter. If we go back to that post and look at the optimization chart for the total investment return as a function of the filter length we see that the smallest filter length of 5 had the best overall return. This suggests that maybe we should consider even smaller filter lengths. Although this suggestion is valid, it won’t be necessary to do so because of the costs of doing business.

The Costs Of Doing Business

In the Quantitative Process – Part I we left out the costs of slippage and commissions from our discussion. Slippage is the difference in the price you get when your order goes through compared to the price you see when you place the order. Combined with commissions, for a liquid ETF and stock a reasonable amount for this cost is 0.20% per round trade (buying and selling). If we include these costs in our optimization calculations we get the following results:

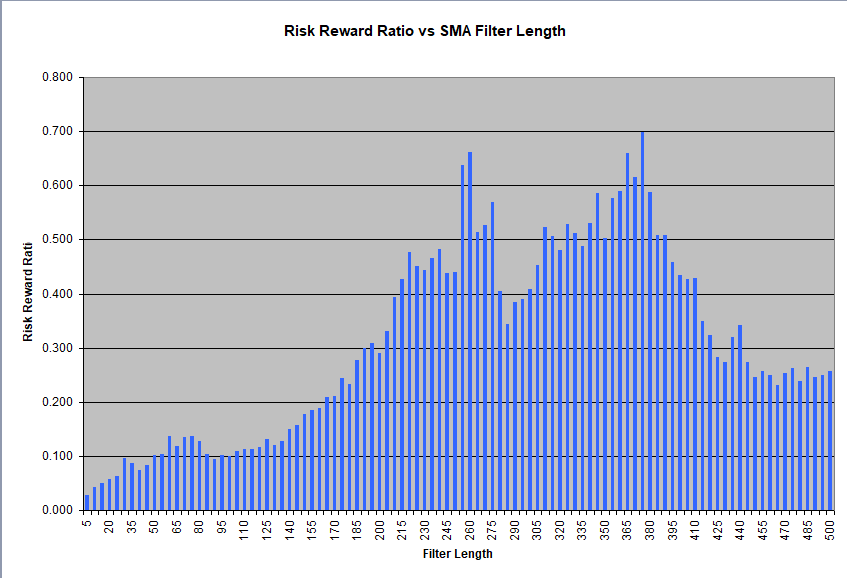

As can be seen by comparing the Investment Return chart above with its counterpart in The Quantitative Process – Part I, strategies with a lot of trades will have a bigger portion of their total returns lost to slippage and commission costs when compared to strategies that trade less often. Thus summarizing our results we get:

| SMA | Return | Trades | Days In | CAGR | Max DD | RR |

| 5 | 369% | 1993 | 9421 | 2.33% | -87.46% | 0.027 |

| 375 | 7,383% | 115 | 12,419 | 6.65% | -9.53% | 0.698 |

| NA | 13,338% | 1 | 16,859 | 7.59% | -56.78% | 0.133 |

This shows that slippage and commission costs had a huge effect on the SMA (5) approach and a smaller effect on the SMA (375) approach. For a complete list of all variations please click here.

It is worthwhile noting here that slippage and commission costs are one reason why it is harder to make money day trading than swing trading. With day trading not only do you have a bigger hurdle to overcome as your costs are higher, but you also have less market movement on average as your time period is smaller.

Choosing a Good Strategy

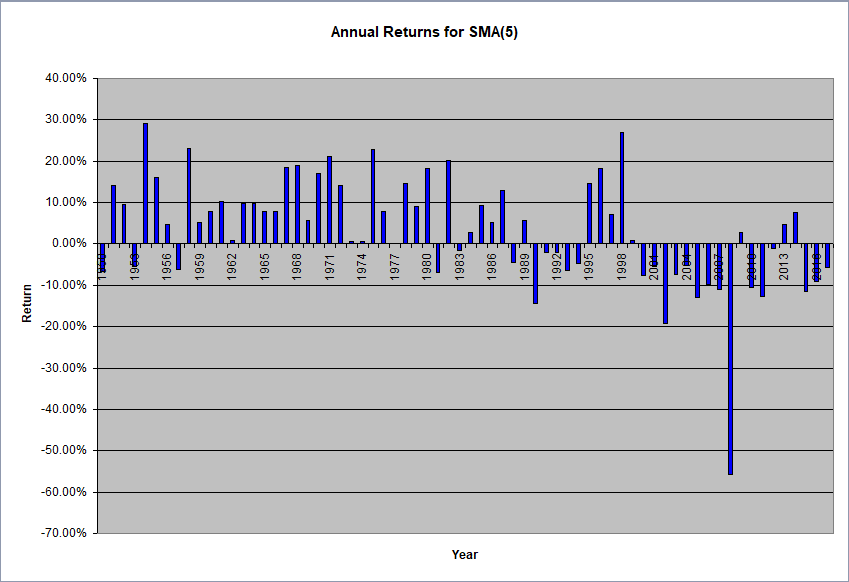

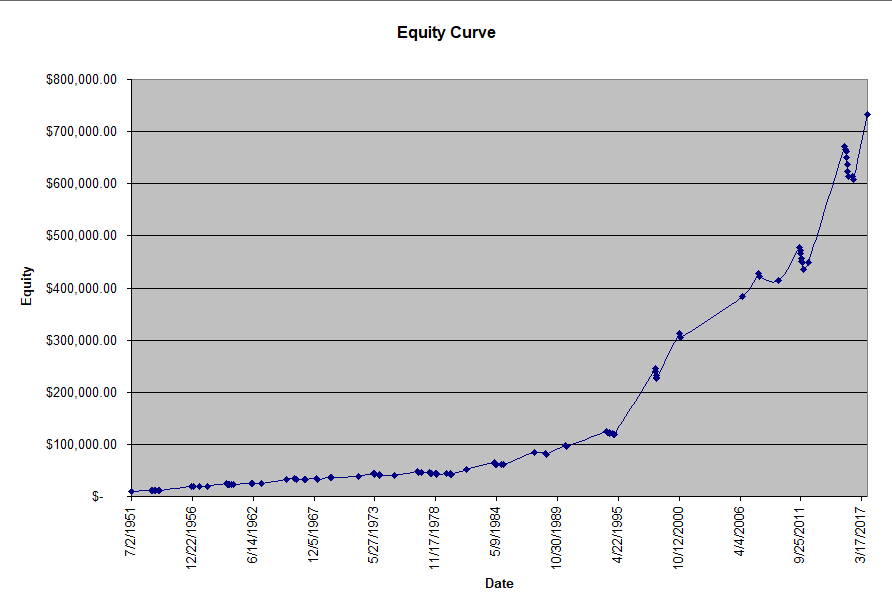

In our example in The Quantitative Process – Part I we ran our tests over a 67 year period, from 1950 to 2016. Let’s have a closer look at how the strategy performed year to year. As a first step, let’s use the SMA (5) variation since it has the largest number of trades. This is illustrated in the image below.

Looking at the above chart one can clearly see that there are two distinct zones, before the year 2000 and after the year 2000. Before the year 2000, the strategy had some losing years but made money overall. In fact it had a CAGR of 7.38%. (For a full list of results from 1950 up to 1999 click here.) After the year 2000 the strategy had more losing years than winning years and it included a very bad year, 2008. These observations are further confirmed when we look at the drawdowns as outlined in the table below. In particular the first row shows that this strategy has not yet recovered from the biggest drawdown that started on 2000830.

| Drawdown | Start | Max DD | End |

| -68.81% | 20000830 | 20110930 | 20161228 |

| -13.90% | 19870915 | 19871127 | 19890523 |

| -12.89% | 19900607 | 19910114 | 19910214 |

| -10.05% | 19731001 | 19731221 | 19741016 |

| -8.98% | 19611128 | 19620620 | 19621119 |

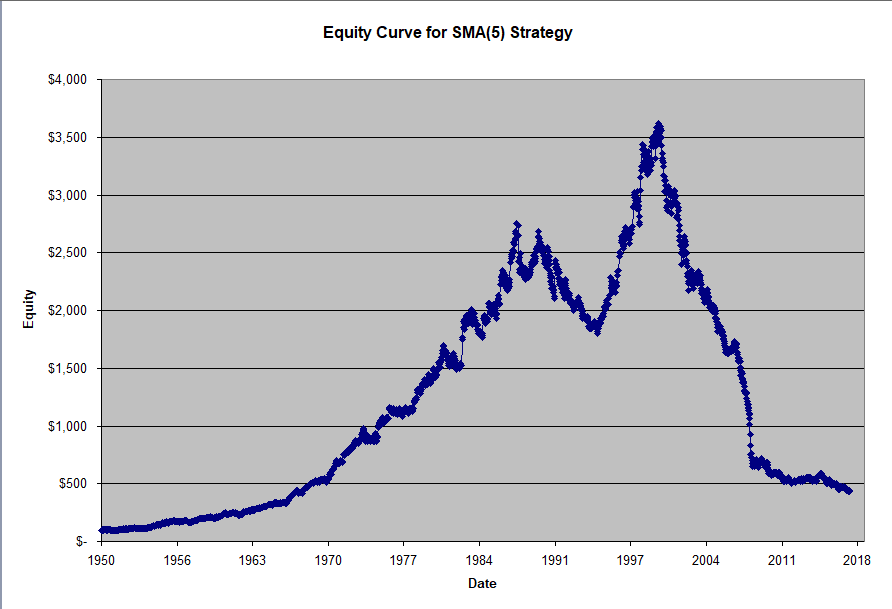

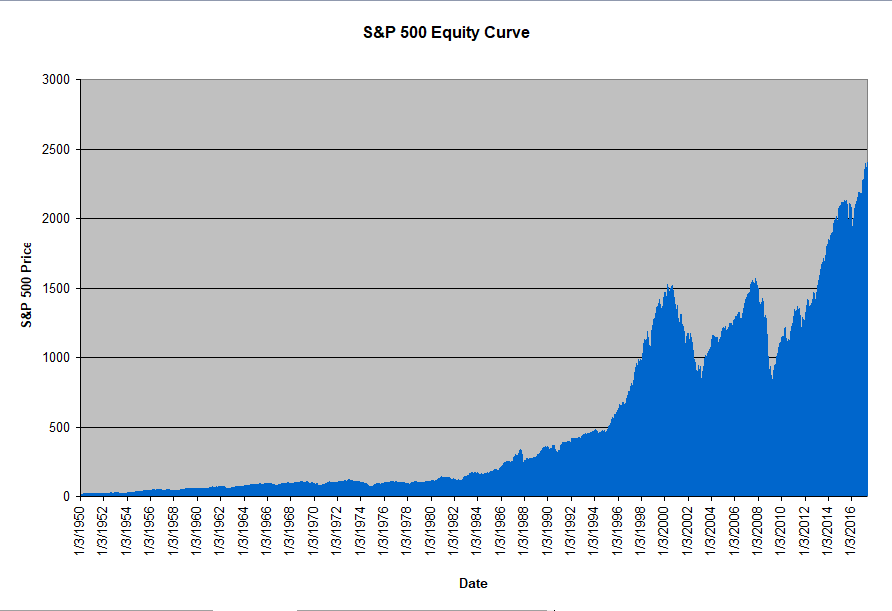

This is also evident in the equity curve below.

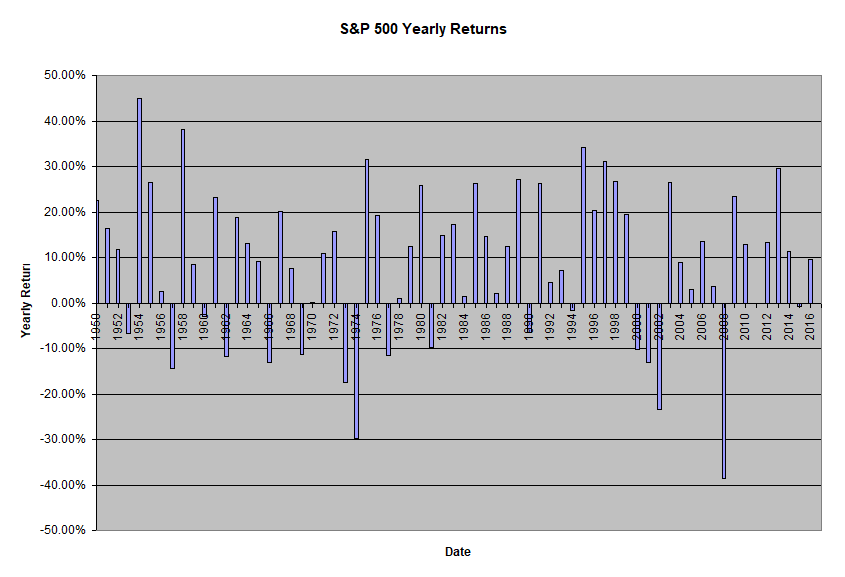

If we look at the annual returns for a buy and hold strategy in the S&P 500 we see no clear distinction before and after the years 2000 as illustrated below.

The above images suggest that although using the SMA (5) to enter and exit the market might have been a good idea in the past it is no longer making money. Despite the fact that there have been no obvious changes in the market as far as average annual returns are concerned, there have been many underlying changes that make this approach to trading the market no longer viable. Such changes include trading volume, high frequency trading, algorithmic trading, low discount brokers, hedge funds, investment regulations etc…

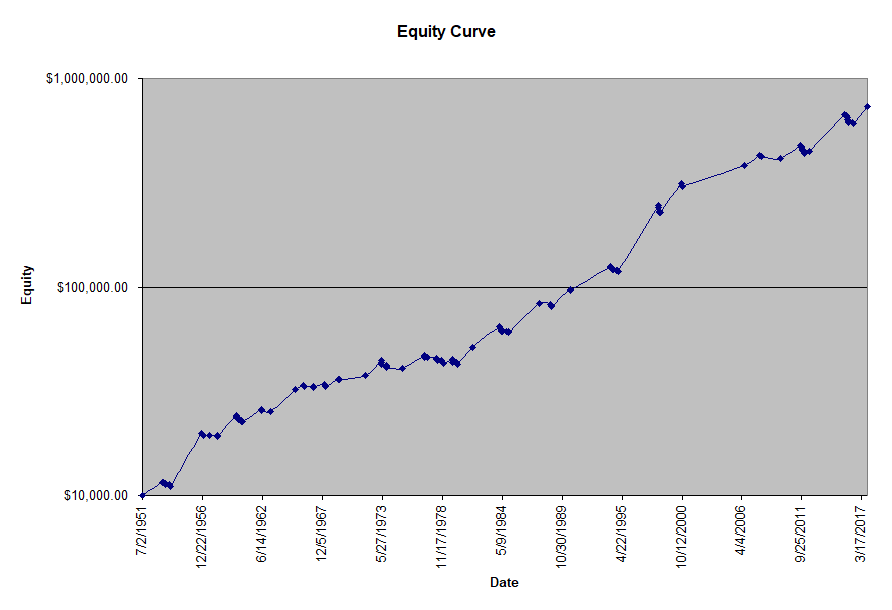

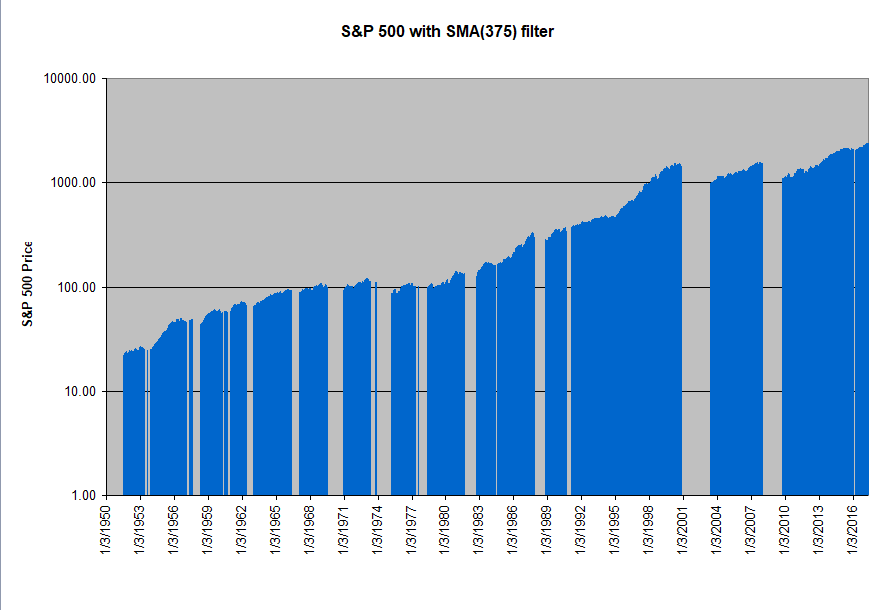

Now let’s have a look at the SMA (375) equity curve.

The above pictures show no significant changes in the equity curve characteristics over time. This is further supported by the drawdown table below which shows the 5 biggest drawdowns.

| Drawdown | Start | Max DD | End |

| -9.53% | 19770324 | 19800414 | 19810826 |

| -9.45% | 20150821 | 20160624 | 20170921 |

| -8.55% | 20110804 | 20111214 | 20150821 |

| -8.46% | 19730425 | 19750318 | 19770324 |

| -7.94% | 19980831 | 19981013 | 20001010 |

If we have a look at the S&P 500 equity curve with the SMA (375) filter applied to it we see that in essence this filter puts us in cash during the elongated drawdown years. In particular, this filter is effective at avoiding the strong market crashes such as those of 2001 and 2008.

The above paragraphs suggest that the SMA (375) strategy is a good strategy going forward as it allows us to make good returns on our investment while limiting our downside during market crashes.

Looking Into The Future

The main reason we develop quantitative investment strategies is so that we can use them to make money going forward. For this to be viable, we need to have a reasonable expectation that the market behavior is going to be somewhat similar in the future to what it has been in the past. The above discussion looked at two variations of the same strategy using a filter length of 5 and 375 respectively. From our observations we conclude:

- A good strategy identifies particular characteristics of the underlying market and exploits them to make money. Although SMA (5) and SMA (375) are two parameters of the same strategy, they are looking at very different market characteristics and can thus be looked at as different strategies if one wants. While SMA (5) is trying to take advantage of short term momentum in the market caused by recent news and events, SMA (375) is taking a longer term approach and ignores shorter term news and the associated price movements in favor of bigger trends as effected by macro-economic conditions.

- Past performance is not necessarily indicative of future results. This statement is included in all financial literature but it is rarely explored. The SMA (5) study above showed how despite working for 50 years, the strategy is no longer viable. When the underlying market characteristics change then the strategy might no longer be viable. That said, it did work for 50 years which is a significant amount of time for any investor.

To see some of the quantitative strategies I trade as part of my portfolio please visit the Investment Strategies page.